Many people find themselves in need of quick cash to cover unexpected expenses or emergencies. Payday and title loans are two common options for obtaining the necessary funds. You must understand the differences between the two types of loans before deciding.

A payday loan is a short-term repayment of the borrower’s next payday. Such loans have high-interest rates and fees and lead to a cycle of debt if not paid back promptly. On the other hand, a title loan involves using an asset, such as a car or motorcycle, as collateral for a larger sum of money. Title loans have high-interest rates and fees but offer more flexibility regarding repayment schedules and amounts borrowed.

Payday Loans: What You Need To Know

Payday loans are short-term, high-interest loans designed for individuals who need immediate financial assistance. Borrowers use such loans for unexpected expenses or emergencies and obtain them quickly with minimal requirements. The application process for a payday loan is relatively simple.

- The borrower fills out an online application that requires basic personal information such as name, address, and employment status.

- The borrower must have a steady source of income and a checking account to be eligible for a payday loan.

- The approval time for a payday loan varies depending on the lender but usually takes only a few minutes.

- Repayment options for payday loans include paying back the full amount and interest on the due date or renewing the loan by paying just the interest fee. Note that such high-interest rates lead borrowers into difficult debt cycles to break free from.

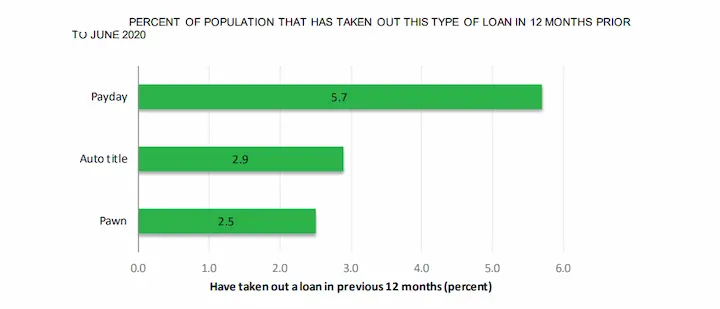

7 in 10 of those who take out payday loans use them for regular recurring expenses such as utility bills and rent payments, according to Credit Summit.

| Detail | Value |

|---|---|

| Number of Americans who use payday loans per year | 12 million |

| Number of payday loan storefronts in the US (as of 2021) | 23,000 |

| Typical duration of debt for a payday borrower (in months) | 5 |

| The average size of a payday loan | $30,000 |

| Percentage of payday loan borrowers who use loans for bills | 7 out of 10 (or 70%) |

| The total amount of fees paid in payday loans per year | $375 |

| Average fees paid by payday lenders to borrow $375 | $520 |

| The typical duration of debt for a payday borrower (in months) | $9 billion |

Title Loans: Understanding The Basics

Title loans, known as auto title loans or car title loans, are a type of secured loan in which the borrower uses their vehicle’s title as collateral. The amount borrowed depends on the value of the vehicle and its condition. Lenders generally offer 25-50% of the vehicle’s total value.

Applicants must meet certain requirements, such as having a clear title to their vehicle (meaning it is fully paid off), proof of income, identification documents, and insurance coverage on the vehicle to qualify for a title loan. Borrowers apply for a title loan at a lending institution either online or in person once they meet the qualifications.

Advantages of Title Loans.

- Quick access to cash. Title loans provide fast cash when needed.

- No credit check is required. Title loans do not require one, unlike traditional loans where credit checks are mandatory.

- Flexible repayment options. Borrowers have various payment options that best suit their financial situation.

Disadvantages of Title Loans.

- High-interest rates. Interest rates are much higher than other types of personal loans due to the high-risk nature of the loan type.

- Possibility of losing your car. You may lose ownership of your car if you default on payments.

- Extra fees. Lenders usually include extra fees like processing fees and late payment penalties.

Alternatives to Title Loans.

- Personal Loans

- Credit Union Loans

- Friends & Family Loan

- Payday Alternative Loans (PALs)

Loan Amounts And Repayment Terms

- Loan amounts and repayment terms vary depending on the type of loan taken.

- Payday loans are short-term loans, usually under $1,000, with a higher interest rate than traditional ones.

- Title loans involve giving the lender a lien on your vehicle’s title, usually for larger amounts than payday loans.

- Repayment terms for both types of loans are usually relatively short, usually within a month.

- Payday loan interest rates are as high as 400% APR, while title loan interest rates vary depending on the lender.

- Read the agreement carefully to understand the full terms and conditions of the loan.

Loan Amounts

Regarding loan amounts, payday, and title loans have restrictions and limitations. Payday loans are smaller than title loans due to the eligibility requirements that borrowers must meet. Lenders usually require proof of income, identification documents, and a checking account for payday loan applicants. Borrowers must only obtain as much money as they can repay from their next paycheck. It means the maximum amount for payday loans is limited to a few hundred dollars.

On the other hand, title loans offer much higher maximum loan amounts than payday loans since they use vehicles as collateral. The value of the vehicle determines how much lenders give in funding.

Borrowers must know that title loan repayment terms vary depending on state regulations and lender policies. Various states allow extensions or rollovers, while others do not. APRs and finance charges are high with both types of loans, so borrowers must carefully review all options before applying for short-term financing.

Repayment Terms

Borrowers must review the loan amounts and repayment terms regarding short-term loans. Short-term loans have higher interest rates and fees than traditional bank loans, so understanding the repayment terms is key to avoiding defaulting or incurring extra costs.

One key aspect of repayment terms is if it contains early repayment or rollovers. Most lenders charge late fees if a borrower misses their payment deadline, while others allow them to pay off their loan earlier without any penalties.

Various states permit rollover options that extend the loan’s due date but add more interest and fees to the total cost. Understanding such options helps borrowers determine which lender offers flexible repayment terms that fit their financial situation.

Interest Rate

Borrowers must pay attention to the interest rates lenders charge for short-term loans. Interest rates significantly affect the total cost of borrowing and vary from lender to lender. Borrowers must compare annual percentage rates (APR) among various lending options to determine the most affordable rate.

Borrower qualifications influence the interest rate offered by lenders. People with good credit scores qualify for lower interest rates than those with poor ones. Most lenders charge hidden fees that increase the borrower’s costs despite low-interest rates.

State regulations impact how much a lender must charge regarding maximum interest and other fees. The loan duration is another factor affecting the total amount paid in interest charges. Longer durations are likely to result in higher overall costs than shorter ones.

Collateral Requirements: Payday Loans Vs. Title Loans

Listed below are the collateral requirements of payday loans vs. title loans.

- Payday loans are short-term loans that do not require any form of collateral. Lenders grant such loans based on a borrower’s creditworthiness rather than any tangible asset.

- On the other hand, Title loans are secured loans, meaning that they require a form of collateral, such as a car or other valuable item, to get approval. Collateral acts as a form of security to guarantee loan repayment.

- Title loans require the borrower to possess a valuable asset used as collateral. Payday loans do not require any form of collateral but are more difficult to qualify for, given the reliance on creditworthiness.

Payday Loan Collateral

The eligibility requirements are relatively simple when it comes to payday loans. Borrowers need proof of income and a checking account to qualify for short-term loans. Title loans require collateral in the form of a vehicle, but payday loans do not have any specific collateral requirements.

The lack of collateral has its risks for borrowers. Payday loan interest rates are extremely high, sometimes reaching triple digits in annual percentage rate (APR). They face steep fees and penalties that further exacerbate their financial situation if borrowers cannot repay their payday loans on time.

Borrowers must carefully weigh the risks and benefits before opting for a payday loan over alternatives like personal or credit cards. On the other hand, title loans require borrowers to use their vehicles as collateral to secure financing. The process involves an appraisal of the vehicle’s value, after which the lender offers a loan amount based on that value.

Title loans seem appealing due to their relative ease of approval and larger loan amounts compared to payday loans, and they carry a significant risk. Borrowers who default on their payments lose their vehicles altogether.

Given such tradeoffs between different types of short-term lending options available to consumers, individuals facing financial difficulties must carefully assess all factors before deciding how best to manage debt and improve their financial health.

Title Loan Collateral

Borrowers are required to use their vehicles as collateral to secure financing. Lenders put a lien on the borrower’s vehicle and hold onto its title until you pay the loan. Borrowers must have a lien-free title to qualify for a title loan.

The appraisal process involves an assessment of the vehicle’s value, after which the lender offers a loan amount based on that value. Borrowers who opt for title loans must understand their responsibilities regarding repayment.

Failure to make timely payments results in the repossession of the borrower’s vehicle by the lender. It is worth noting that each state has different laws regarding repossession, so borrowers must familiarize themselves with such laws before agreeing to any terms with a lender. Borrowers must carefully weigh the risks and rewards of obtaining a title loan before committing.

Comparing Collateral Requirements

The most significant factor to assess is collateral requirements when borrowing money. Payday loans and title loans are two lending options that differ regarding their collateral requirements. Payday loans do not require any assets as collateral, but title loans rely heavily on the borrower’s vehicle as a form of security.

Title loan borrowers must have a lien-free car title to qualify for financing, while payday loan borrowers only need proof of income and identification. Repayment flexibility varies between the two types of loans depending on state regulations and lender policies.

Interest Rates And Fees

Collateral requirements are just one aspect of comparing payday loans and title loans. Another key factor is the interest rates and fees associated with such lending. Both types of loans are expensive, but they differ regarding how much borrowers pay in interest and other charges.

Title loans carry higher interest rates than payday loans because they require collateral (i.e., the borrower’s car), making them a lower risk for lenders. Title loan interest rates compound more frequently than payday loans, increasing costs. Payday loan fees quickly increase if borrowers cannot repay their debt on time or must continuously borrow money to make ends meet.

You must compare APRs between different lenders before committing to any loan. Watch out for hidden charges, such as loan origination fees or prepayment penalties, that significantly increase the overall cost of borrowing funds.

Making The Right Choice For Your Financial Situation

Payday loans are short-term loans that are due on your next payday. Borrowers use them for emergency expenses such as car repairs or medical bills. The advantage of a payday loan is you don’t need collateral to secure the loan, but the downside is that they have high-interest rates and fees.

On the other hand, title loans require borrowers to use their vehicles as collateral. The amount you borrow depends on the value of your car, and repayment periods are usually longer than payday loans. You risk losing your vehicle if you default.

Both types of loans have eligibility criteria based on income and employment status, but credit scores aren’t considered when applying for them. You must carefully assess all factors before deciding which type of loan is best for your financial situation.

There are alternative options available besides payday or title loans. If you’re struggling financially, you must try negotiating payment plans with creditors or seek assistance from non-profit organizations like credit counseling agencies or consumer finance protection bureaus.

Such alternatives are not immediate fixes for urgent needs but offer long-term benefits towards better budgeting practices while avoiding unsustainable debt traps in future endeavors. Weighing all options help make informed decisions tailored toward individual circumstances without sacrificing financial stability.

Conclusion

You must understand the differences between payday loans and title loans before deciding. Payday loans are smaller with shorter repayment terms, while title loans offer higher loan amounts but require collateral in your car or other vehicle. Take the time to research both options and make an informed choice if you need quick cash. Review interest rates and fees as they add up quickly, leaving you in even more financial trouble.

Frequently Asked Questions

How do payday loans differ from title loans?

Payday loans use income as collateral while title loans use the borrower’s car title as collateral for the loan amount.

What are the eligibility requirements for a payday loan vs. a title loan?

Payday loans require income, ID, and a bank account. Title loans require income, ID, and owning a car fully or nearly paid off.

What is the typical repayment period for payday loans and title loans?

Payday loans are due in full on the borrower’s next paydate, usually 2-4 weeks. Title loans are 30 days on average but can be extended.

Are the interest rates higher for payday loans or title loans?

Title loan rates are lower on average, around 25% monthly. Payday loan rates can be over 400% APR.

What assets or collateral are needed for a title loan compared to a payday loan?

Payday loans require only income as collateral. Title loans use the borrower’s car title as collateral if the loan is unpaid.