Payday loan companies have become increasingly popular in recent years. According to a survey by the Pew Charitable Trusts, over 12 million Americans get payday loans every year with an average of 375% interest rate. The statistic alone paints a vivid picture of how necessary the financial solutions are for borrowers who need help accessing traditional forms of credit.

The purpose of a payday loan company is simple: providing short-term cash advances to individuals who need fast access to money before their next paycheck arrives. These types of businesses tend to serve people with bad or no credit histories and borrowers looking for emergency funds that can’t be met through other means. The process is relatively straightforward. Customers fill out an online application at the store, including information about employment status and income level. They will receive either instant approval or feedback within a few minutes if extra documents are required. Customers pay back the amount and any fees accrued when their next paycheck arrives once approved.

Payday loans have risks since high-interest rates can make them difficult to repay on time without incurring extra charges. They can provide much-needed relief during financial hardship when more conventional options aren’t available, offering consumers the sense of belonging that comes from knowing someone has their back in moments of crisis. The article further details what makes up a normal payday loan company operation today to better understand both sides.

Key Takeaways

- Payday loan companies provide short-term loans secured against the borrower’s next paycheck, normally with high-interest rates attached, and require proof of income, bank statements, and other supporting documents before approving a loan application and providing details on repayment terms, such as fees or penalties if payments are missed.

- The steps involved in how payday loan companies work include submitting an application, loan approval, fund transfer, and fees and penalties, and borrowers must borrow from reputable companies licensed in their respective jurisdiction, pay off debts promptly, and avoid falling further into debt cycles.

- Individuals must research companies, understand terms, and build relationships while keeping track of upcoming payments, never borrowing beyond one’s means, and take responsible actions that set up borrowers for long-term success to get the most out of payday loans. It is necessary to compare lenders, determine eligibility criteria, review the repayment period, and read through the small print before selecting a payday loan company.

- Payday loans are a fast option for short-term cash but carry high-interest rates and exorbitant fees that lead to further financial problems.

- Alternatives such as installment loans, online banks, and peer-to-peer lending platforms offer more flexibility regarding repayment and are a better option for individuals looking for temporary funds.

- It’s necessary to research all the terms and conditions thoroughly to avoid potential pitfalls before entering into any contract with payday loan companies. Understanding the loan agreement is necessary to avoid hidden fees and interest rates.

Definition Of Payday Loan Companies

It is understandable to be skeptical of payday loan companies, as they have earned a reputation for predatory lending practices. Nonetheless, it is necessary to understand the institutions and how they operate to make an informed decision. A payday loan company provides short-term loans secured against the borrower’s next paycheck, normally with high-interest rates attached. The lender requires proof of income, bank statements, and other supporting documents before approving a loan application and provides details on repayment terms, such as fees or penalties if payments are missed. These loans help individuals cover unexpected expenses until their next paycheck arrives but must not be examined as a long-term solution due to their high-interest rates. Payday loan companies tend to target borrowers who lack access to traditional banking services and use aggressive marketing tactics to entice vulnerable populations into getting significant amounts of debt without fully understanding the consequences. Consumers must research all available options carefully before making any financial decisions.

How Payday Loan Companies Work

Payday loan companies are a helpful source of quick cash for borrowers needing immediate financial assistance. The companies assess borrowers’ creditworthiness and offer short-term loans based on their findings. It is necessary to approach the loans responsibly to avoid falling into debt cycles.

Listed below are the steps involved in how payday loan companies work.

- Apply. Borrowers must apply with the lender to obtain a payday loan. The application includes information such as proof of income, bank statements, and other financial details to assess the borrower’s creditworthiness.

- Loan approval. After reviewing the borrower’s application and financial details, the lender assesses if the individual is eligible for a quick loan. If approved, the lender agrees upon terms, including repayment plans and interest rates.

- Fund transfer. Funds are transferred into the borrower’s account within 24 hours once all the required documents have been submitted and agreed upon by both parties, making it one of the fastest ways to access extra money when needed.

- Fees and penalties. Payday lenders impose fees for late payments or defaults on repayments, similar to traditional lending institutions. The penalties usually carry extra charges beyond what is expected from conventional banks due to the risk of being unable to recover the entire amount lent at once.

- Responsible borrowing. It is necessary to note that borrowers must borrow from reputable companies licensed in your respective jurisdiction. It is necessary to pay off debts promptly to avoid falling further into debt cycles.

Choosing The Right Payday Loan Company

Choosing the right payday loan company is an intimidating task. Access to funds quickly is necessary, so you must select the most suitable lender for your needs in a financial emergency. Visualize yourself being in control of finding a reliable payday loan provider who offers you money without charging excessive interest rates or hidden fees. Here are four key points to review when selecting a payday loan company.

- Compare lenders.

Research different payday loan companies online to guarantee you find the best deal that fits your budget and requirements. Assure yourself to read reviews from other customers, as it gives you an insight into what kind of service they provide before committing to any agreement. - Find out about eligibility criteria.

Different companies have rules regarding lending terms and conditions, so guarantee you understand the criteria fully before applying for a loan. You must meet certain criteria to be eligible for a loan with them, even if they advertise competitive rates. - Review the repayment period.

Note that other lenders require borrowers to repay loans quickly, which puts pressure on your finances if you cannot pay back by the due date. Look around and compare each lender’s policy on late payments, too, as hefty charges are associated with missed deadlines. - Read through the small print.

Before making any decisions, it’s necessary to thoroughly read through all documents provided by potential lenders, including contracts, agreements, and terms & conditions. Pay close attention to fees and extra costs initially obscure or advertised upfront.

You must rest assured knowing that your decision is informed and secure by considering the tips when searching for a suitable payday loan company. You can confidently select someone who meets your circumstances while providing peace of mind in knowing that if anything unexpected arises during repayment periods, help is available whenever needed.

Getting The Most Out Of Payday Loans Companies

Navigating the payday loan company terrain feel like a minefield, but with careful strategizing, it is viable to optimize the outcome. It requires understanding what constitutes a reputable source and how to get the most out of them once engaged. The guidelines help jumpstart any journey, like laying down railroad tracks.

- Researching Companies

A good place to start is by researching different companies that offer loans in your area. Review factors such as interest rates, repayment terms, customer service ratings, and online reviews before deciding. - Understanding Terms

Guarantee you have read all documents carefully and understand exactly what the loan entails. Ask questions if there’s anything you don’t fully comprehend or if extra information is needed about fees or other aspects of the agreement. - Building Relationships

Payday lenders require repeated borrowing due to their short-term nature. The condition means lower costs over time and better customer experiences overall. Building relationships with certain companies is beneficial for future needful requirements.

It’s necessary to keep track of upcoming payments to make them on time; late payments result in extra charges piling up quickly and creating more financial distress than when first starting. Never borrow beyond one’s means nor agree to a loan whose stipulations will not be met without bringing hardship upon oneself; the strategies must lead towards debt freedom instead of further entrenchment within it. Taking responsible actions now sets up borrowers who take advantage of payday loans for long-term success later.

Legality Of Payday Loans

Payday loans have become increasingly popular over the years as a means of short-term credit. Payday loan companies offer quick financial relief for borrowers facing unexpected expenses or an emergency like a lifeboat in turbulent seas. But t is necessary to understand that not all payday loan businesses operate legally according to state and federal regulations.

The legality of such services varies by jurisdiction. Many states have imposed restrictions on lenders and borrowers, such as caps on interest rates and fees, limits on loan amounts, or required repayment terms. Other states allow them, while others do not. Federal law regulates payday lending practices, with laws like The Truth in Lending Act stipulating how much information must be disclosed when advertising or offering payday loans. Many cities and counties have passed ordinances that further restrict the activities of payday loan companies within their borders.

Understanding what is involved with payday loan transactions, including viable consequences if you default, is key to making informed financial decisions. It is necessary to research any potential lender before getting a payday loan to guarantee they are operating lawfully and abiding by the applicable regulations. Before returning to such service, consumers must review other options available, such as seeking assistance from family members, friends, charities, or social programs.

Types Of Payday Loans

Payday loans have become popular for people who need quick cash to cover unexpected expenses or financial emergencies. The types of payday loans include short-term, long-term, and online ones. Understand the different types of payday loans and the risks involved before getting a loan while payday loans offer fast access to funds.

Short-Term Payday Loans

Short-term payday loans are the most common type available in the market. Short-term payday loans involve small amounts of money borrowed over a short period, usually 15 days to one month. The borrowed amount is usually determined by income level, credit rating, and employment status. Payday loans offer quick access to funds, while loans have higher interest rates than other forms of credit.

Long-Term Payday Loans

Long-term payday loans are another type of payday loan available in the market. These loans usually have longer repayment periods than short-term payday loans and stretch beyond one month. Payday loans have higher interest rates, while payday loans offer more repayment time. The amount borrowed depends on factors such as income level, credit rating, and employment status, as with short-term payday loans.

Online Payday Loans

Customers can now apply for payday loans online through websites or mobile apps, making the process even more convenient. It is necessary to exercise caution when applying for loans online and to verify that the lender is reputable and trustworthy.

Secured Vs. Unsecured Payday Loans

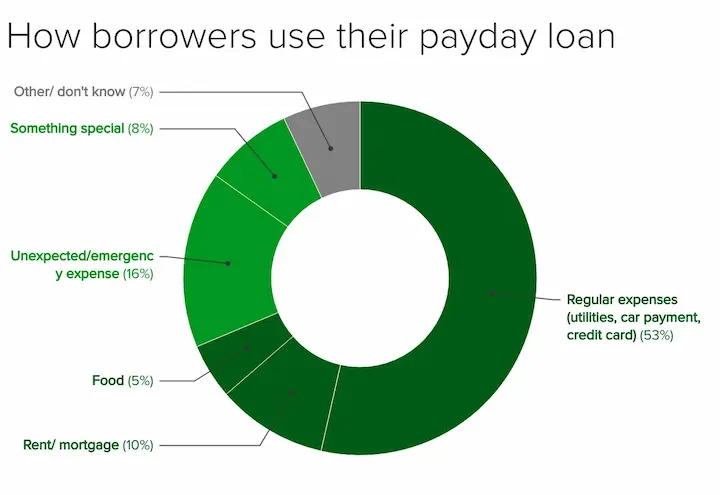

Payday loan companies are becoming increasingly popular, with 62% of borrowers using them for emergency expenses like car repairs and medical bills. Secured vs. unsecured payday loans offer customers different levels of risk when it comes to borrowing money.

A secured loan requires collateral in exchange for the loan amount. The condition is any valuable item, such as a vehicle or property, the lender holds that until payment has been received in full. This type of loan offers more protection against defaulted payments since lenders have something they repossess to cover their losses. An unsecured loan does not require collateral and relies solely on the borrower’s creditworthiness and ability to repay secure repayment. These types of loans have higher interest rates than secured loans due to the increased risk the lender takes.

Payday loan companies provide customers with quick access to funds without going through a lengthy application process or waiting days for approval. Depending on their current financial situation and goals, customers must assess risks and rewards before getting either type of payday loan from a company. It’s necessary to compare fees between providers so borrowers get the best deal viable for their needs.

Repaying A Payday Loan

Repaying a payday loan is a necessary examination for any individual seeking short-term financial assistance. Here are three key points to help borrowers better comprehend the process and its associated examinations. You must understand the repayment terms imposed by lenders and the potential consequences of non-payment.

Most payday loans have a relatively short repayment period compared with other types of borrowing. The condition includes processing fees and extra charges for early installment payments. The condition requires prompt payment once due or late fees are incurred. Having enough funds available on the agreed-upon date is necessary. Secondly, other lenders offer various deferment forms if necessary, such as extending the loan term or allowing more time before the first installment is due. Thirdly, it is necessary to review extra costs beyond interest rates when determining how much money must be set aside each month to repay the loan.

Individuals must make informed decisions about their financial obligations and plan accordingly to effectively manage their finances throughout the loan agreement by understanding all aspects of a payday loan’s associated fees and repayment guidelines.

Alternatives To Payday Loans

Payday loan companies are like a ship in the night; they offer quick cash but with the looming risk of financial insecurity. Alternatives to payday loans provide better options for consumers needing short-term credit options.

One alternative is installment loans, which allow borrowers to make fixed payments until their debt is paid off. Payday loans generally have lower interest rates than traditional ones, giving borrowers more flexibility regarding repayment terms. There are less stringent requirements for eligibility, such as having a higher minimum income or longer employment history than most payday lenders require. Other online banks and peer-to-peer lending platforms have similar offerings that help individuals needing temporary funds without incurring excessive costs.

The alternatives are invaluable when getting an unexpected expense that needs immediate attention. They have many advantages compared to getting a payday loan and must be examined before considering such an expensive option. The alternatives usually carry better long-term benefits, but they potentially save you money in the long run, something that is never achieved through relying on payday lenders alone.

Pros And Cons Of Payday Loan Companies

Payday loan companies offer short-term, high-interest loans to eligible borrowers. Such financial services are an alternative to more conventional forms of credit and have both advantages and drawbacks for consumers.

The primary advantage of payday loan companies is quick access to funds when other sources are unavailable or impractical. For example, suppose an individual needs money quickly due to a medical emergency or unexpected expense. In that case, they can receive funds from a payday lender with fewer bureaucratic hurdles than lenders by more traditional lending institutions. Payday lenders don’t require collateral like a house deed or car title like other borrowing options.

Potential downsides for individuals who use the firms include exorbitant fees associated with repayment that put people into further debt, even bankruptcy in extreme cases. The condition leads to further difficulties in obtaining necessary funds when needed. Many jurisdictions limit the amount borrowed from such providers and the number of times it is done before legal action must occur.

Payday loan companies provide a unique service but must only be used after careful examination and comparison against other available alternatives. It is advisable to research thoroughly all terms related to getting such loans before entering into a contract with a provider.

Advantages Of Payday Loans Companies

Payday loan companies have become increasingly popular in the age of modern technology. Payday loans offer a unique advantage over traditional banks and lenders regarding speed and convenience from an economic standpoint. Borrowers access funds quickly with minimal paperwork. Below are the key benefits that businesses provide.

- Fast approvals

Like other loan providers, most payday loans are approved within minutes or hours instead of days or weeks. - Low-interest rates

Many payday loan companies offer lower APRs than traditional credit cards or bank loans, while interest rates vary depending on the lender. - Flexible repayment plans

Payday loan companies allow customers to repay their loans over time in flexible installments rather than requiring them to make one lump sum payment at once. - Bad credit accepted

Many payday loan companies do not require potential borrowers to have good credit scores for approval. The condition makes it easier for borrowers with poor credit histories to get the money they need in a financial emergency. - No collateral required

Most payday loan providers check employment status and income level before approving a borrower’s application, unlike other types of lending, which require assets as security.

Payday loan companies benefit borrowers who need more cash due to unexpected expenses or emergencies. The businesses provide individuals and families with quick access to much-needed funds without using more expensive options such as getting high-interest debt from traditional banks or relying on less reliable sources of financing like family members or friends with such lenient requirements and fast processing times. They give people greater flexibility in managing their finances without worrying about lifelong debt cycles. They allow consumers to spread their payments over multiple months while avoiding long-term commitments.

Disadvantages Of Payday Loans Companies

The irony is used to point out the absurdity of a situation. The thought is certainly true when it comes to payday loan companies. Payday loans offer quick access to money for borrowers with financial difficulties yet have high-interest rates and other fees that make them an expensive option in the long run. Unsurprisingly, there are disadvantages associated with using payday loan companies with such drawbacks.

Payday loans are issued by non-traditional lenders operating outside of existing regulations which means consumers need to be properly protected from predatory practices or scams. Many payday loan companies have very strict repayment requirements, making it difficult for people facing financial hardship to meet their obligations on time and pay off their debts without accruing further costs through late payment charges. Borrowers resort to getting more than one loan at a time due to the need for ongoing cash flow because they are short-term loans, thus incurring even more debt.

The above factors contribute towards creating a cycle of debt that is hard to break without external assistance or help from family and friends, something many don’t have access to. The factors only ever be used as a last resort since they carry significant risks and potential consequences if payments are not met on time or in full. Payday loan companies provide fast access to funds during times of need at the same time.

Understanding The Loan Agreement

Payday loan companies are a helpful financial solution for borrowers needing short-term cash assistance. Understanding the terms and conditions of payday loans is necessary to avoid potential pitfalls. A recent survey found that out of 1,000 payday loan borrowers, 40% reported needing to be better informed about their rights as consumers or what they agreed to when they signed the loan agreement.

It’s necessary to read all the details before signing any contract to guarantee you understand exactly what you are getting into. Hidden fees or interest rates are attached if you do not take the time to carefully review the details while lenders make promises of quick money and no credit checks. Knowing your rights as a consumer help protect you from predatory lending practices such as high-interest rates and rollover clauses where debt accumulates quickly due to escalating payments over an extended period.

It is paramount that every borrower has a complete understanding of their legal responsibilities before entering into any contractual arrangement to get the most benefit from a payday loan company. Being aware of common traps like misstated payment amounts and other deceptive tactics allows customers to make educated decisions regarding their finances without putting themselves at risk. Taking advantage of available resources such as online reviews and consumer protection organizations helps borrowers become better equipped for making sound decisions when dealing with payday loan companies.

Reasons To Use Payday Loan Companies

Payday loan companies provide short-term loans to help people manage their finances in times of need. But why do people turn to the services?

One advantage is that they offer convenience and speed. Unlike traditional banks or lending institutions, payday loan companies make funds available within 24 hours. The advantage makes it an attractive solution for an emergency expense or unanticipated bill. Another benefit is that most payday lenders have lenient eligibility criteria compared to other forms of credit. It’s viable to qualify even if you need a perfect credit record or a reliable income source. Other states allow borrowers to roll over existing loans without penalty fees, providing extra flexibility if circumstances change unexpectedly.

Payday loan companies thus represent an accessible financial resource in times of need, offering both ease and expedience with minimal bureaucracy and prerequisites attached. Customers enjoy more favorable terms than what is offered by alternative options such as overdrafts or bank loans. Therefore, it comes as no surprise that organizations remain a widely used choice among individuals who require access to immediate funds.

Reasons To Avoid Payday Loans Companies

Symbolic of a debt trap, the payday loan company has become familiar to many people facing financial hardship. A seemingly easy and accessible form of borrowing money in times of need, the establishments quickly lead to disaster if not used carefully or cautiously.

Understanding when it’s best to avoid getting a high-interest short-term loan from such companies is one powerful thing that anyone dealing with financial difficulty must understand before attempting to use them as a resource. Reasons why someone wishes to stay away from payday loan companies, include the astronomical interest rates they charge, the lack of long-term planning options available for borrowers already struggling financially due to their current debts, and the potential negative impact on credit scores if payments are missed.

Interest on payday loans is very high compared to more traditional forms of lending, such as banks and credit unions. It means any borrowed funds are significantly more expensive than other methods. Most lenders only offer repayment plans for up to two weeks, preventing individuals from planning future payments. Missing payments seriously damage a person’s credit score, compounding financial difficulties.

Payday loans seem like a tempting solution, but it’s necessary to note that there are better alternatives and that using them rarely solves anything in the long run for borrowers looking for help managing their finances in difficult times.

Payday Loan Costs

| Payday Loans | Credit Cards | |

|---|---|---|

| Maximum loan fee (per $100) | $10 to $30 | – |

| Typical loan fee (per $100) | $15 | – |

| Maximum loan amount | Capped | – |

| APR | Almost 400% | 12% to 30% |

| State laws | Permit, regulate, or prohibit | – |

| Protections for servicemembers | Federal Military Lending Act (MLA) | – |

| MAPR cap for servicemembers | 36% | – |

| Other limitations on fees | Yes | – |

The table above compares payday loans and credit cards regarding loan fees, maximum loan amount, annual percentage rate (APR), state laws, and protections for service members, as reported by the Consumer Financial Protection Bureau.

Payday loans are short-term loans that have to be repaid within two weeks, and they are used by people who need quick cash but have poor credit. The payday loan cost varies by state, but many states cap the loan fees and maximum loan amount. The loan fee is $15 per $100 borrowed, which results in an APR of almost 400%. In contrast, credit cards have APRs ranging from 12% to 30%.

State laws play a role in regulating payday loans. Other states do not permit payday lending, while others permit or regulate it. More information is available from state regulators or attorneys general in states that allow payday lending.

Servicemembers and their dependents are protected under the federal Military Lending Act (MLA), which sets a cap of 36% on the Military Annual Percentage Rate (MAPR) and limits what lenders charge for payday and other consumer loans. Servicemembers contact their local Judge Advocate General’s (JAG) office to learn more about lending restrictions and use the JAG Legal Assistance Office locator to find help.

Final Thoughts

Payday loan companies are a viable option for borrowers needing quick cash, but it is necessary to understand their implications and drawbacks. Borrowers must know they are not the most cost-effective form of borrowing as payday loans carry high-interest rates. Regulations vary between states, so it is necessary to guarantee that any payday lender complies with local laws. Understanding the terms of the agreement is necessary when getting a payday loan. Resolving the issue quickly and efficiently helps avoid further financial difficulties if they occur.

Statistics show that over 12 million Americans get payday loans each year. The figure demonstrates just how popular such services have become in recent years as individuals seek alternative forms of credit. There is an increasing demand for reliable lenders who offer competitive prices and clear repayment terms for their customers.

Payday loan companies provide consumers with an easy way to access money in times of need, but caution has to be exercised when using one of the services. Borrowers must have read through all relevant information before signing up for a loan agreement and research available options thoroughly to guarantee they get the best deal.

Frequently Asked Questions

How do payday loan companies work?

Payday lenders offer short-term, high-cost loans that borrowers promise to repay out of their next paycheck, often at interest rates from 200% to 500% APR.

What are the typical interest rates charged by payday loan companies?

Payday lenders commonly charge $15-$30 per $100 borrowed which translates to an APR of 200% to 500% on a typical 2-week loan term.

Are payday loan companies regulated by the government?

Payday lenders are regulated at the state level to varying degrees, but are not banned federally, leading to inconsistent oversight nationwide.

What are the risks associated with borrowing from payday loan companies?

Risks include getting trapped in repeat borrowing cycles with fees exceeding the original loan, loss of bank account/wages, damaged credit, and high stress.

How do payday loan companies compare to traditional banks and credit unions?

Payday loans have much higher interest rates and poorer terms than loans from banks/credit unions, but may approve applicants banks deny.