Payday loans are a form of short-term lending that has become increasingly popular in recent years. Such loans offer borrowers quick access to cash, with little or no credit check required. Payday loans have high-interest rates and fees, making them an expensive way to borrow money.

One issue with payday loans is the practice of rollovers. A rollover occurs when a borrower is not able to repay their loan on time and instead chooses to extend it for another period by paying only the interest owed. It is a convenient solution at first glance. Still, it quickly leads to a cycle of debt as interest continues to accrue, and the borrower finds themselves unable to pay off the original loan amount.

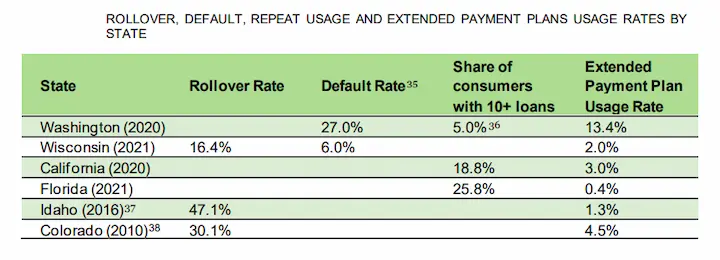

The Mechanics Of A Payday Loan Rollover

Understanding a payday loan rollover is key for borrowers struggling to make payments. A rollover occurs when a borrower is not able to repay the full amount of their loan on the due date and requests an extension from the lender. The extension comes at a cost, as interest rates and fees continue to accrue during the rollover period. Rollover consequences are severe, leading to increased debt and financial hardship for borrowers.

Lenders impose higher interest rates or stricter repayment terms during the extended period, making it even more difficult for borrowers to pay off their loans. Borrowers must understand their lender’s rollover policies and check if requesting an extension is worth the potential long-term costs.

It is the borrower’s responsibility to verify they clearly understand their obligations before obtaining any loan. Approximately 80% of payday loans are taken out within two weeks of paying off a previous payday loan, according to LendEdu.

| Detail | Value |

|---|---|

| Average payday loan fee for borrowing $375 | $520 |

| The average fee charged by a payday lender for a two-week loan | $55 |

| Payment required from the next paycheck for the average loan | $430 |

| Percentage of gross pay required to repay average loan | 36% |

| Percentage of payday loans taken out after paying a previous loan within two weeks | 80% |

| Percentage of payday loans taken out by repeat borrowers within a year | 75% |

The Risks Of Rollovers

Payday loan rollovers are short-term, high-interest loans offered to people needing quick cash.

- They have high-interest rates, making it difficult for borrowers to repay the loan on time.

- A borrower’s lack of financial literacy leads them to obtain multiple payday loans, creating an unsustainable debt cycle. It results in borrowers entering a debt cycle that is difficult to escape.

High-Interest Rates

The consequences of a payday loan rollover are severe, especially when high-interest rates are involved. Predatory lending practices target vulnerable individuals who do not have the financial literacy to understand the risks associated with borrowing irresponsibly.

Such borrowers become trapped in a cycle of debt where they continually roll over their loans, accruing more interest each time. There are consumer protections in place, such as limits on interest rates and regulations on how many times you must roll over a loan to protect consumers from predatory practices,

Individuals borrow responsibly and fully understand the terms of any loan they take out. Increasing financial literacy and educating borrowers on the risks associated with payday loans makes it easier to work towards reducing the number of people caught in the vicious cycle of rollovers and high-interest rates.

Unsustainable Debt Cycles

Transitioning into the subtopic of unsustainable debt cycles, understand that rollovers lead individuals to financial instability. The inability to repay loans results in borrowers obtaining more loans and falling deeper into debt. The cycle is challenging to break without external assistance such as credit counseling or budgeting tips.

Borrowers must borrow responsibly by only borrowing what they need and ensuring they have the means to pay back their loans on time. Financial education is a key tool in preventing unsustainable debt cycles from occurring. Providing savings strategies and educating individuals on responsible borrowing habits makes it easy to help them avoid payday loans altogether or use them more effectively when necessary.

Credit counseling services assist people struggling with debt in creating a plan for repayment and managing their finances better overall. Reducing the number of individuals caught in unsustainable debt cycles requires a combination of consumer protections, increased financial literacy, and access to resources for people trapped in such a situation.

Alternatives To Payday Loans And Rollovers

There are many payday loan alternatives that borrowers must know of.

- Credit Unions offer a viable alternative to payday loans and rollovers due to their low-interest rates, flexible repayment terms, and services such as financial education and counseling.

- Financial planning is another option for people looking for alternative payday loans and rollovers. Financial planning enables individuals to set goals, create budgets and identify potential sources of extra income.

- Budgeting is key to managing finances instead of high-cost loan options such as payday loans and rollovers. Creating a budget helps individuals to track their income and expenses and identify areas where they must cut back to save money.

- Budgeting helps individuals to save money for large purchases and plan for future financial goals. It helps them to identify and prioritize spending, enabling them to make sound financial decisions.

Credit Unions

Credit unions are a viable option for individuals who want to avoid the high-interest rates associated with payday loans and rollovers. The primary benefit of credit unions is that they offer lower interest rates on loans than traditional banks. They operate as non-profit organizations, allowing them to reinvest profits into their members through better loan options and higher savings yields.

Membership requirements for credit unions tend to be less strict than big banks, making them more accessible to people from different backgrounds.

Credit unions play a key role in community involvement. Credit union members have a say in how their institution operates and even participate in decision-making processes through voting rights. Such a level of engagement fosters a sense of belonging among members, creating a supportive network that goes beyond just financial services.

Financial Planning

Financial planning is a key aspect of managing one’s finances, and credit unions offer resources to help their members plan for a secure financial future. It includes guidance on budgeting basics, saving strategies, credit management, investment planning, and retirement planning.

Offering such services at little to no cost enables credit unions to empower individuals with the necessary tools to make informed decisions about their money. Credit unions prioritize education as part of their mission to promote financial wellness among their members.

They provide workshops and seminars that cover various topics, such as debt reduction and wealth building. It helps individuals improve their financial literacy and fosters a sense of belonging within the community by bringing people together who share similar goals and values.

Budgeting

Credit unions offer budgeting resources that help individuals avoid financial pitfalls when transitioning to alternatives to payday loans and rollovers.

Budgeting is one of the most fundamental aspects of personal finance, yet it’s overlooked or poorly executed. Credit unions provide tools and guidance on creating a budget that aligns with an individual’s long-term financial goals while allowing for spending flexibility.

It includes educating members on savings strategies such as setting aside emergency funds, frugal living tips, and debt management techniques. Promoting sound financial planning practices through budgeting education enables credit unions to empower their members to make informed decisions about their money.

They encourage a sense of community by bringing together individuals with similar values toward financial responsibility. As a result, credit unions support alternative lending options that are more affordable and sustainable for long-term financial stability.

How To Avoid The Debt Cycle

Borrowers must implement several budgeting tips to avoid the debt cycle caused by payday loan rollovers.

- First, you must create a realistic budget and stick to it. It involves tracking all expenses and cutting back on non-essential purchases.

- Building an emergency fund provides a safety net for unexpected expenses and reduces the need for borrowing in the first place.

- Credit counseling services are useful for people struggling with debt. Such organizations offer advice on managing finances, negotiating with creditors, and creating repayment plans.

- Debt consolidation is an option for combining multiple debts into one payment with lower interest rates or monthly payments.

- Improving financial education through resources such as books or online courses helps individuals make better decisions about their money in the long term.

- Taking proactive steps toward financial stability enables borrowers to break free from the cycle of payday loan rollovers and improve their overall financial health.

Seeking Help With Debt Relief

The borrower is not able to repay the loan on time and must extend the term by paying extra fees in such situations. It leads to an endless cycle of borrowing and rolling over loans that is difficult to escape. Knowing how to deal with payday loan rollovers is key to avoiding getting caught in a debt cycle. Review the following tips to prevent such from happening.

- Seek Debt Counseling – Talking with a financial counselor helps you understand your debt management options.

- Explore Credit Repair Options – There are ways to repair it so you qualify for better interest rates if missed payments or defaults have damaged your credit score.

- Review Bankruptcy Options – Filing for bankruptcy is the best way to get out of debt and start fresh.

- Consolidate Loans – Loan consolidation allows you to combine multiple debts into one monthly payment at a lower interest rate.

Conclusion

Payday loan rollovers are a common practice among borrowers who find themselves unable to repay their loans on time. It seems like a helpful solution but leads to even more debt and financial instability. The mechanics of a payday loan rollover involve extending the repayment period of a loan by paying extra fees or interest.

There are risks associated with payday loans and rollovers you must review, like any form of borrowing. Alternatives are available for people seeking short-term financing without using such high-risk options. Understanding such factors and avoiding the debt cycle enables individuals to regain control over their finances and pursue long-term stability.

Frequently Asked Questions

How does a payday loan rollover work?

A payday loan rollover occurs when a borrower cannot repay the loan by the due date and takes out a new payday loan to cover the old one. The borrower pays only the fees due on the original loan and extends the due date.

Are payday loan rollovers legal in my state?

Payday loan rollovers are legal in some states but restricted or banned in others. You should check the laws in your state to determine the legality and any restrictions, such as limiting rollovers to a maximum number.

What are the potential consequences of a payday loan rollover?

Potential consequences of a payday loan rollover include getting trapped in a cycle of debt, fees accumulating to exceed the original loan amount, damage to your credit score, increased stress, and risk of falling behind on other bills or expenses.

Can I avoid a payday loan rollover if I can’t repay the loan on time?

You may be able to avoid a payday loan rollover by communicating with the lender early about an extension or payment plan, borrowing from family/friends, using a credit counseling agency, taking out an installment loan, or using a credit card if available.

Are there alternatives to payday loan rollovers for managing financial emergencies?

Alternatives to payday loan rollovers include borrowing from family/friends, credit cards, credit counseling programs, small emergency loans from employers, non-profit organizations or banks, debt management plans, budgeting apps, or seeking additional income sources.