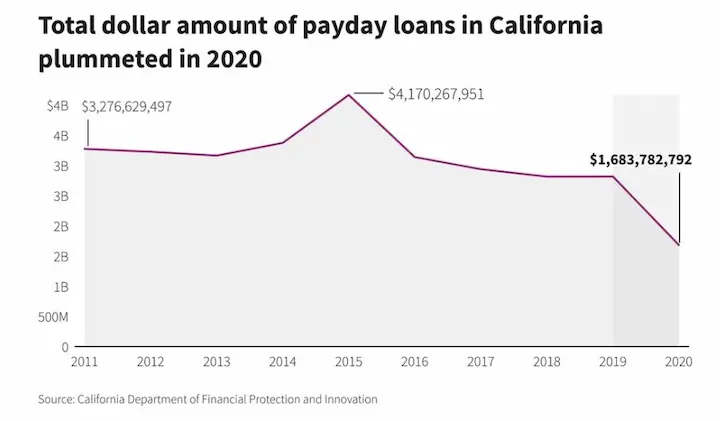

The payday loan industry in California has grown significantly in recent years. Payday loans are short-term and unsecured, with high-interest rates and fees, making it challenging for borrowers to repay them on time. Many individuals find themselves trapped in a cycle of debt where they take new loans to pay off old ones.

Consolidating payday loans is an effective way to manage multiple debts and reduce overall interest rates. It involves taking a single loan with a lower interest rate and using it to pay off all existing payday loans.

Consolidating payday loans requires careful evaluation of various factors such as eligibility requirements, lender options, repayment terms, and potential risks involved. The article provides comprehensive guidance on consolidating payday loans in California while highlighting essential tips that borrowers must know before embarking on the process.

SUMMARY

- Payday loans are short-term and high-interest loans that trap borrowers in a cycle of debt if not managed responsibly.

- Consolidating payday loans is an effective way to manage multiple debts and reduce interest rates.

- California has state and federal laws regulating payday loans to protect borrowers from predatory lending practices.

- Payday loans have strict repayment timelines, and failure to repay on time has serious consequences.

- The maximum APR for payday loans in California is 460%, and lenders charge up to $17.64 per $100 borrowed.

- Violations of payday loan laws in California are subject to penalties under Title 10 of the U.S. Code.

Understanding Payday Loans In California

Payday loans are short-term loans that have become increasingly popular across the United States. Payday loans in California are regulated by both state and federal laws to provide borrowers with protection against predatory lending practices. Payday lenders still charge high-interest rates and fees, making it difficult for borrowers to repay their loans despite legal regulations.

Payday loans in California have an interest rate of up to 460% APR and must be repaid within two weeks to one month. Repayment plans vary between lenders but usually involve automatic withdrawals from the borrower’s bank account on the due date. Borrowers have rights under California law, including the right to rescind the loan within 24 hours without penalty and request an extended repayment plan if they cannot afford to repay the loan in full.

What Are Payday Loans?

Payday loans are short-term and high-interest loans that offer quick access to cash when needed. A payday loan must be repaid within a month, providing an excellent solution for people who have unexpected bills or need money between paychecks.

Payday loans are short-term loans with high-interest rates that require full repayment within two weeks to one month. Payday loans have strict repayment timelines and are easier to get out of if borrowers stay caught up on payments.

Payday loans are short-term unsecured loans with small amounts of money borrowed, due on the borrower’s next payday or within a few weeks, and have high-interest rates and fees. Payday loan lenders do not require collateral, but lenders ask for post-dated checks or authorization to access the borrower’s bank account.

Payday loans meet emergency financial needs such as unexpected bills or medical expenses. Payday loans are very expensive due to the high-interest rates, and borrowers easily fall into debt traps if they fail to repay the loan on time.

How Do Payday Loans Work?

Payday loans are like a lifeboat to many people, providing access to short-term funds when the cost of living is too high. Payday loans provide an invaluable lifeline for people who need it most through quick approval and a simple application process. Understanding how payday loans work is necessary so borrowers can make informed decisions regarding their financial needs.

The first step in understanding payday loans is learning about eligibility criteria. Applicants must complete an online form with information about finances and supporting documentation. The lender assesses the borrower’s ability to repay the loan on time after submission. Funds are made available within 24 hours via direct deposit into a bank account.

Repayment terms vary depending on the amount borrowed but generally involve one payment at a specific date determined by both parties before the disbursement of funds. The repayment must include interest fees calculated according to the terms of each contract if not paid within the timeframe, charges apply. Making payments on time is necessary to avoid late fees or default on your loan agreement, and failure to do so has serious consequences that impact future loan options from lenders.

What Is The Maximum APR For Payday Loans in California?

APR equals 460%, according to the Center for Responsible Lending 2019. APR is based on the average rate for a $300 loan advertised by the largest payday chains or as determined by state regulators where applicable, according to UStatesLoans.

The fee is $17.64 per $100.00 borrowed. Finance charges must not exceed 15% for every $100 of the amount advanced. Interest is not allowed if a lender willingly agrees to prolong the payment according to the law.

Provisions of § 987 of Title 10 of the U.S. Code as amended by 126 Stat. One thousand seven hundred eighty-five states that anyone who violates the provision or a provision of Part 232 violates division 10 of California Deferred Deposit Transaction Law.

| Scenario | Value | Explanation |

| Maximum APR for payday loans in California | 460% | Lenders in California are allowed to charge up to $17.64 per $100 borrowed, which means you have to pay $52.92 in fees if you borrow $300. |

| Fee per $100 borrowed | $17.64 | California law states that finance charges and fees must not exceed 15% for every $100 of the amount advanced, which means you are charged up to $45 in fees if you borrow $300. |

| Maximum finance charges and fees | 15% | Lenders are not allowed to charge interest if they agree to prolong the payment according to California law, but no specific value is associated with the scenario. |

| No interest on extended payment | N/A | Anyone who violates the provision or a provision of Part 232 violates Division 10 of California Deferred Deposit Transaction Law is subject to penalties as per the §,987 of Title 10 of the U.S. Code as amended by 126 Stat. 1785. The value associated with the scenario is not specified. |

| Violation penalties | As per §,987 of Title 10 of the U.S. Code | Anyone who violates the provision or a provision of Part 232 violates Division 10 of California Deferred Deposit Transaction Law is subject to penalties as per the § 987 of Title 10 of the U.S. Code as amended by 126 Stat. 1785. The value associated with the scenario is not specified. |

What Is Loan Consolidation?

Debt consolidation, like a conductor bringing together an orchestra, combines multiple loans into one harmonized payment plan. It is done through various means, such as balance transfer credit cards or personal loans with lower interest rates and longer payment terms.

The main objective of loan consolidation is to simplify financial planning by streamlining debts into a single manageable monthly payment, reducing the chances of missing payments, and improving credit scores over time due to consistent, timely repayments. Debt consolidation allows borrowers to benefit from lower interest rates which lead to savings in the long run.

What Is the Average Fee for Loan Consolidation?

The average fee for loan consolidation is about 4% if you choose to get a debt consolidation loan and 2.55% if you get a balance transfer credit card. You need to consider the fees and the APR on your new loan or credit card when deciding if debt consolidation is worth it.

The average APR for a debt consolidation loan is 14.47%. The average introductory APR for a balance transfer credit card is 0% for 13 months, followed by the regular APR, according to WalletHub.

| Type of Debt Consolidation | Average Fee | Average APR | Introductory APR | Length of Introductory Period |

| Debt Consolidation Loan | 4% | 14.47% | N/A | N/A |

| Balance Transfer Credit Card | 2.55% | Variable | 0% | 13 months |

How To Consolidate Payday Loan in California?

Obtaining a debt consolidation loan is an effective solution to pay off debts in a more manageable way. Debt consolidation is merging several debts into one payment plan with lower interest rates and longer repayment terms.

The debt consolidation option simplifies monthly bills and reduces overall interest costs, allowing individuals to save money in the long run. Understanding its various aspects and requirements is necessary before applying for a debt consolidation loan. The article explores how to consolidate payday loans in California.

- Assess Your Financial Situation. Assessing your financial situation is the first step toward obtaining a debt consolidation loan. It involves examining your budgeting goals and identifying how much you can pay monthly for your debts. You must know how consolidating your debts affects your credit score and explore different repayment plans that align with your financial objectives. Debt counseling is helpful in understanding the options available for consolidating your loans and managing your finances effectively. Financial security requires careful planning and assessment of one’s current financial state.

- Understand The Benefits Of Debt Consolidation. Exploring options for debt consolidation involves researching different types of loans, such as home equity loans, balance transfer cards, or personal loans. Evaluating the benefits of debt consolidation include assessing the potential savings on interest rates and fees and the effects of lowered monthly payments. Comparing rates among lenders involves researching the Annual Percentage Rates (APR) and the repayment terms for different loans.

- Shop Around For The Best Loan. The next step in obtaining a debt consolidation loan is to become an astute researcher, like a detective on the hunt for clues which means evaluating lenders and their offerings by comparing interest rates, fees, and repayment terms. It involves researching requirements such as credit scores, income levels, and collateral options. Weighing all options against one another help determine which path is best suited to individual needs while exploring alternatives like balance transfer cards or home equity loans that seem attractive at first glance.

- Compare Interest Rates And Fees. When obtaining a debt consolidation loan, comparing interest rates and fees from multiple lenders is necessary. Applying for multiple loans allows borrowers to assess which lender offers the best deal regarding APRs and repayment options. Budgeting for debt repayment plans is necessary before applying for a consolidation loan, as it helps determine how much money is allocated toward monthly payments. Consolidating debts impacts credit scores positively or negatively depending on payment history and credit utilization rate. Understanding loan repayment options and choosing the one that aligns with financial goals while minimizing negative impacts on credit scores is necessary.

- Prepare The Required Documentation. After exploring options and evaluating alternatives, you have decided that a debt consolidation loan is the best way to manage your debt. Preparing the required documentation before applying for such a loan is necessary, including proof of income, employment status, credit score, and outstanding debts. It’s necessary to budget wisely, and you must afford the monthly payments on the loan. You can be better equipped to obtain a debt consolidation loan that meets your needs and helps you pay off credit cards and small loans effectively by carefully evaluating the factors and preparing all necessary paperwork in advance.

- Apply For A Debt Consolidation Loan. It’s necessary to know various factors that impact the outcome of your application when applying for a debt consolidation loan. One major benefit of consolidating debt is lowering payments by combining multiple debts into one manageable payment plan. It’s necessary to clearly understand your budget and financial goals before applying. Budgeting tips such as reducing unnecessary expenses and increasing income help improve your chances of getting approved for a debt consolidation loan. Another factor to know is the length of the loan since longer terms result in higher interest rates and overall costs.

Advantages Of Consolidating Payday Loan

Loan consolidation is a process through which multiple loan payments are combined, potentially allowing borrowers to lower their overall interest rates or reduce their monthly payments. Consolidating payday loans benefits borrowers by providing a lower interest rate, reducing the number of monthly payments, and simplifying the loan repayment process.

Lowering Interest Rates

One key advantage is the potential to lower interest rates when considering the benefits of consolidating loans. Borrowers can save money over time and reduce their debt by combining multiple high-interest debts into a single loan with a lower interest rate.

The process is facilitated through various ways, such as debt negotiation or credit counseling. Individuals can secure favorable terms and achieve greater financial stability with careful planning and strategic negotiating. Consolidation allows individuals to simplify their finances while lowering monthly payments and reducing the interest paid over time.

Reducing Monthly Payment

Another benefit of consolidating loans is the potential to reduce monthly payments achieved by negotiating a longer repayment term or securing a lower interest rate through credit counseling, as mentioned earlier.

Borrowers free up more cash flow for other expenses and have greater financial flexibility by reducing monthly payment obligations. It’s necessary to note that extending the repayment term result in paying more interest over time despite having a lower monthly payment. Consolidating loans helps individuals achieve greater financial stability while potentially lowering their debt burden and improving their overall quality of life.

Final Thoughts

Payday loans in California are short-term and unsecured loans with high-interest rates and fees that must be repaid within two weeks to one month. Consolidating payday loans is an effective way to manage multiple debts and reduce overall interest rates. Still, it requires careful evaluation of various factors such as eligibility requirements, lender options, repayment terms, and potential risks involved.

Borrowers must understand payday loan eligibility criteria and repayment terms to make informed decisions regarding their financial needs. The maximum APR for payday loans in California is 460%, with lenders allowed to charge up to $17.64 per $100 borrowed, and finance charges must not exceed 15% for every $100 of the amount advanced.

According to California law, lenders cannot charge interest if they agree to prolong the payment. Anyone who violates the provision or a provision of Part 232 violates division 10 of California Deferred Deposit Transaction Law is subject to penalties.

Frequently Asked Questions

What is the process for consolidating payday loans in California?

The process involves working with a debt consolidation company to combine multiple payday loans into one manageable payment through a consolidation loan. The company negotiates with lenders and handles paperwork.

Are there specific eligibility criteria for payday loan consolidation in California?

Basic requirements include being a California resident, having outstanding payday loans that need consolidation, sufficient income to make monthly payments, and providing necessary financial documentation.

How can I find reputable payday loan consolidation companies in California?

Research companies, check the California Department of Business Oversight license lookup, read reviews, verify BBB accreditation, consider nonprofit credit counseling agencies, and avoid companies charging upfront fees.

What are the potential benefits of consolidating payday loans in California?

Benefits include combining multiple payments into one, lower monthly payments, reduced interest rates, avoiding snowballing fees, structured payment plans, improved credit, and focusing on becoming debt-free.

What are the legal regulations and requirements for payday loan consolidation in California?

Regulations include caps on interest and fees, required state licensing, adherence to federal consolidation loan rules, mandatory credit counseling, and prohibited abusive lending practices.