Personal Loan for Debt Consolidation?

No one enjoys being in debt or accumulating it over time. People often find themselves in situations where their finances are out of control and they have a lot of debt. These types of situations are becoming more common. Thinking about your options when going through a financial crisis is important. To get out of debt, one of the best options is debt consolidation.

You can use personal loans to pay off high-interest unsecured debt such as credit card debt. Consolidating your debt can help you pay off your credit card debt and provide a simplified repayment schedule with more favorable repayment terms.

Before deciding whether a consolidation loan for debt is right for you, evaluating your financial situation and goals is important. It can help you save time and money depending on the terms and amount of your debt. Lenders consider different factors during the loan application process, such as your credit reports, current debt, and minimum income requirements.

Online lenders often provide debt consolidation loan options with competitive interest rates. The online application process can be completed quickly, and if you get a loan approval, the loan proceeds could be received in your account within a few business days. However, be aware of the loan agreement, payment terms, and the repayment period.

To find the best debt consolidation loan interest rate and minimum loan amounts, comparing various loan options and debt consolidation lenders is crucial. Remember that late payments can negatively affect your future credit approval and credit decisions. Always make a minimum payment towards your debt payments to maintain a good credit profile throughout the time of application.

When it comes to managing your finances and seeking a personal loan for debt consolidation, location matters. RixLoans is dedicated to helping individuals across the United States regain control of their financial well-being. Below is a comprehensive list of the American states where we operate, providing our tailored debt consolidation solutions to support your journey towards financial freedom.

| Alabama | Alaska | Arizona | Arkansas |

| California | Colorado | Connecticut | Delaware |

| District Of Columbia | Florida | Georgia | Hawaii |

| Idaho | Illinois | Indiana | Iowa |

| Kansas | Kentucky | Louisiana | Maine |

| Maryland | Massachusetts | Michigan | Minnesota |

| Mississippi | Missouri | Montana | Nebraska |

| Nevada | New Hampshire | New Jersey | New Mexico |

| New York | North Carolina | North Dakota | Ohio |

| Oklahoma | Oregon | Pennsylvania | Rhode Island |

| South Carolina | South Dakota | Tennessee | Texas |

| Utah | Vermont | Virginia | Washington |

| West Virginia | Wisconsin | Wyoming |

A debt consolidation loan can positively impact your financial well-being if managed correctly. Consider the type of loan you wish to apply for and the repayment options available. Here are the facts.

What Are the Best Times to Consider a Debt Consolidation Loan?

You can get personal loans for almost any purpose, but you can only use them for debt consolidation. To have favorable terms, one should consider a debt consolidation loan rate when struggling with high-interest credit card balances and when a single debt consolidation loan would streamline multiple debt payment obligations.

Excellent Credit History

Personal loans can be obtained by anyone with any credit rating. However, Harris and Partners recommend that you have a high credit score to get lowest rate interest rates and better loan terms. Some lenders might even consider less-than-ideal credit applicants but may require higher rates or secured loan options.

High-Interest Rates Are a Sign of a High Debt

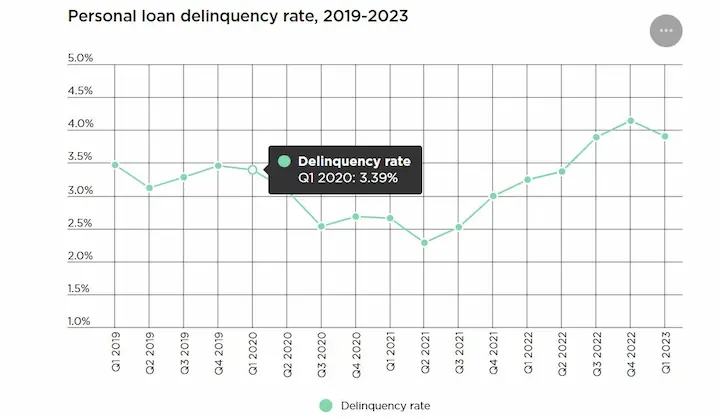

Personal loans have an average personal loan rate of 9.41%, while credit card debt has an average rate of 16%. People who qualify for lower interest rates than they currently pay should consider consolidating their debts to save money over the long term. Rates for debt consolidation vary depending on a variety of factors, such as credit score, income, and loan amount.

A Repayment Plan Is Available

When considering debt consolidation loans, finding a single loan with a fixed repayment schedule that fits your monthly expenses is important. This allows borrowers to manage their debt payment obligations more efficiently. Remember that some lenders may offer variable interest rates or have prepayment penalties tied to their loans, so review the actual loan terms before approval. Additionally, some lenders may charge loan origination fees, which can affect the overall cost of the loan.

Additional Debt Relief Services

For those struggling with bad credit and high-interest loans, other options such as balance transfer credit card or debt relief services can help. Ensure you meet on-time payments and avoid accumulating further debt by cutting down on major purchases. Be cautious of prepayment fees or other hidden costs that may not help reduce your overall loan balances.

Lender Approval and Time of Loan Funding

Lenders review your loan request and may approve it based on several factors, including credit score and income. As a qualified borrower, you may receive loan funding times that vary from a few days to several weeks. Make sure to weigh the pros and cons of each lender before committing to any single loan. Always review the loan agreement thoroughly to understand the specific terms and conditions, such as interest rates, fees, and repayment options.

In conclusion, for borrowers with good to excellent credit, debt consolidation loans can help lower their interest rates and simplify debt payments. Through research and responsible borrowing habits, one can choose the best loan funds and move closer to financial stability. It’s crucial to analyze all options and choose a loan that aligns with your financial goals and repayment capacity to ensure a better financial future.

Credit card debt has one of the most negative aspects. It is revolving. It means you can borrow money and pay it off over time, but there is no repayment plan. You could pay off your debt permanently if you only use your credit card to pay the minimum monthly payment. Personal loans offer a repayment plan to help you quickly escape debt. You can read more.

Although you will see obvious benefits from a consolidation loan for debt, it is not always the best choice to pay off credit card debt. These are:

Your Spending Issues Have Not Changed

Because you can still use your credit card credit, a debt consolidation loan is a good option. Your financial situation can worsen if you accumulate debt from the card you just paid off. Before you consolidate your debt, you should address your spending issues.

Credit Rating Is either Poor or Fair

Financial institutions and credit bureaus use credit ratings to determine the risk of lending money to potential personal loan customers. If your credit rating is poor or fair, you may not be eligible for loan offers with favorable Rates & Terms. Major credit bureaus pay close attention to your income ratio and credit limit when determining your credit rating.

You might consider alternatives such as a credit union or a secured loan. Lines of credit could be viable alternatives, but comparing the cost of credit, loan interest rates, and loan term restrictions is essential.

When seeking credit products for credit card debt consolidation, take note of factors like minimum loan sizes, quick funding, and single payment options. Always carefully read the loan contract and look for hidden fees, payoff penalties, or unfavorable terms. Additionally, be prepared to provide proof of income and other personal information to potential lenders.

As you consider a debt consolidation option, weigh the pros and cons of debt consolidation and assess your ability to repay the loan in monthly installments for the term of the loan. Ensure the actual rate of interest, whether a yearly rate, introductory rate, or variable rate, aligns with your financial goals. By understanding every aspect of the loan, you can make an informed decision and ultimately work towards building credit over a set period of time.

People with poor credit may still get approval for personal loans. However, they must pay higher interest rates and loan costs. These will make it more expensive and sometimes make it difficult for them to repay their loan. Nonprofit organizations and loan consultants may help individuals find the best form of credit with reasonable procedures to assist them in managing their major expenses.

Only a Little Debt

A consolidation loan will not benefit you if you don’t think you can quickly pay off credit card debt in the next six months or a year. You don’t have to take out a personal mortgage if you can pay your monthly credit card bills. Approval for credit may consider factors like customer payment history, annual income, and source of income. It’s important to remember that loan term lengths, payment range, and payment fee may differ among types of loans. Lender charges and credit usage can also play a major role in determining the term of loan and the payment to creditors.

Various options like Credit card refinancing or obtaining extended term loans may be useful in different situations. Within 1-3 business days or hours after loan approval, funds can be available in a borrower’s account, making them a viable option for tackling financial needs in a business day period. The choice of the rate loans can also depend on the credit utilization ratio and whether the provider performs soft credit inquiry during the introductory period.

To facilitate repayments, Automatic payments can be set up, ensuring a better customer service experience and allowing individuals to maintain good credit standings in the long run. Having knowledge of these factors and understanding the major factor that affects each decision about personal loans can empower borrowers to make more informed choices.

Frequently Asked Questions

How does a personal loan for debt consolidation work, and what is its purpose?

It combines multiple debts like credit cards or payday loans into a single personal loan with lower interest to help consumers save money, simplify payments into one monthly bill, and pay off debts faster.

What are the advantages of using a personal loan to consolidate debt compared to other methods?

Benefits include lower monthly payments, reduced interest rates on credit cards, paying off debts faster with a single payment, improving credit through on-time payments, and saving money over the loan’s duration.

Are there specific criteria or qualifications for obtaining a personal loan for debt consolidation?

Typical criteria include a minimum credit score around 580, steady verifiable income, low debt-to-income ratio, and sufficient cash flow to make the monthly consolidation loan payments and cover living expenses.

How can I determine if a personal loan for debt consolidation is the right choice for my financial situation?

Review total costs, projected monthly payments, eligibility requirements, rates compared to your current debts, time to repay, impact on credit, and budget to see if consolidation with a personal loan makes financial sense for your situation.

What factors should I consider when choosing a lender and loan terms for debt consolidation with a personal loan?

Key factors to compare include interest rates, fees, loan amounts, credit score requirements, cosigner options, flexible repayment terms, transparent pricing, and customer service reputation.